7 Things You Should Know Before Getting Into Cryptocurrency

Digital currencies are all the rage right now, and as more and more people get into them, they keep growing in value and fame.

According to current statistics, the average rate of ownership of cryptocurrency is holding steady at 300 million.

This means that even at its downward curve, about 300 million people are trading in cryptocurrency right now. But just because everyone else is doing it doesn’t mean you should jump on the bandwagon – particularly if you don’t know what you’re getting into!

The good news is that understanding the basics of cryptocurrency isn’t that hard.

Things you should know before getting into cryptocurrency

Cryptocurrency has been one of the hottest buzzwords in the past few years, but there’s still a lot of confusion about how it works and why you should care.

What is cryptocurrency? In short, it can be everything from a business opportunity to an investment fad, depending on who you ask.

The process of buying digital currency involves transferring funds from your bank account or credit card into your brokerage account. At this point, you’re ready to buy some coins.

There’s no intermediary involved; all transactions take place between users directly.

This decentralization means there’s less risk of fraud or identity theft than when using a centralized service like PayPal or Venmo. This is a big selling point for cryptocurrency’s popularity.

While people often start trading cryptocurrency as an investment vehicle, that’s usually not what keeps them coming back.

In fact, this article will take you through all that you need to know about cryptocurrency before you invest any money into it.

Let’s get started!

1. Time your investments right

Cryptocurrencies are digital assets that have their own network. The value of these assets fluctuates with time (and other factors) and can be volatile.

However, they’re also built on blockchain technology and therefore have real-world applications outside of investments or trading.

This means you can use them to pay for goods and services, or they may even be able to store your data securely or offer something like a prediction market platform.

If you’re interested in getting involved with digital currency as an investment or trade opportunity — for example, if you would like to buy Ethereum or Bitcoin, make sure to do thorough research.

Keep up-to-date on relevant news and announcements so you know when major changes happen within each cryptocurrency community.

When planning your initial buy, aim for larger targets instead of day trades if possible; at least hold onto your investments long enough to see some significant gains.

And don’t let short-term volatility keep you from continuing to invest over time.

Remember that most digital currencies will increase in value over time due to growing demand from investors and traders alike.

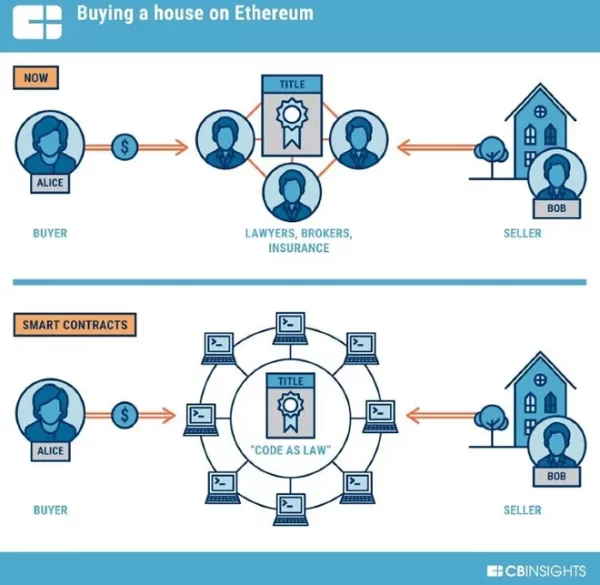

2. Use Ethereum smart contracts

In order to understand Ethereum and its smart contracts, you first need to wrap your head around a pretty big concept.

It’s not enough to simply own a digital currency, such as Bitcoin or Ethereum. You also have to be able to send it to other people—otherwise, what good is it?

The way cryptocurrencies work today is that they use a third party (known as a miner) to serve as an intermediary.

Miners essentially verify each transaction before adding it onto the public ledger (this ensures that all transactions are being conducted fairly and ethically).

However, some of these miners act dishonestly by allowing users to push through dishonest transactions. Thus, acquiring bitcoin for themselves instead of processing honest ones.

Smart contracts eliminate miners from cryptocurrency transactions altogether by putting them on a blockchain network.

Smart contracts are pieces of code that automatically execute when certain conditions are met.

This effectively makes cheating impossible because no one can tamper with what’s been put into writing.

3. Build your own cryptocurrency

There are over 1,000 digital currencies or cryptocurrencies, and they can be used as a means of transferring money between two parties.

However, their value fluctuates with supply and demand. Incredibly, with proper research, starting your own cryptocurrency is possible.

This process involves creating a business plan (business objectives) before even getting into technology (coins/tokens).

There are three essential parts to launching your own coin:

- Building its infrastructure

- Writing a white paper (for developers)

- Designing an ICO campaign for potential investors.

- The right consensus algorithm

- Picking the right blockchain platform to launch your cryptocurrency

- Design of professional website/ mobile application

For example, if you want to start a decentralized system based on blockchain technology and you want all nodes in your network to reach consensus without trust then you will need a consensus algorithm such as proof-of-work.

And if you want to build smart contracts using Ethereum platform then you should choose Ethereum Virtual Machine.

And lastly, designing websites/mobile apps is necessary because people won’t buy something that doesn’t look good or professional enough.

4. Join a crypto community

A community of crypto enthusiasts can be a great resource to help you as you become more familiar with cryptocurrency.

If you’re looking for ways to make money, start your own business, or expand your knowledge of how Bitcoin and other cryptocurrencies work, joining a crypto community is a good way to do that.

Get connected with others on forums like BitcoinTalk, Coindesk, or Reddit.

Just remember: while they may be eager to help newcomers learn about cryptocurrency and get involved, these communities are often filled with people who are also trying to sell things and promote their products.

Always be wary of unsolicited advice from someone whose motivations for giving it may not be 100% honest.

5. Try multiple trading strategies

The cryptocurrency market is still new. But trading has become so popular that people are devising strategies to capitalize on buying and selling certain coins at a certain time.

Some of these strategies include day trading, which involves watching currencies 24/7 to find low-risk entry points.

Night trading, where you watch cryptocurrencies late into the night after major moves.

And a fluctuating strategy, which means riding out big price swings with no interest in short-term gains or losses.

Another strategy is to get into holding some of your coins for longer periods of time instead of hours or days—sometimes even months or years!

It’s all about managing risk, finding your sweet spot, and keeping an eye on opportunities with staying power. Not sure what cryptocurrency is right for you?

Talk to others who are already involved: Chances are there’s someone you know who owns or trades cryptocurrency.

Ask them how they got started, if they have any tips for first-timers, and whether they could offer any insight into how you can learn more.

And then take their advice! A little research can go a long way toward making your first foray into cryptocurrency less intimidating and more fruitful.

6. Pay attention to bearish and bullish patterns

Bearish and bullish patterns are a great way to gauge crypto market sentiment.

Bearish patterns, or candlesticks that point downward, suggest that an asset is oversold and due for a reversal. For example, a hammer candle indicates selling pressure has cooled off, which suggests that investors could be gearing up to buy into a downtrend.

Bullish patterns, like bull flags or inverted hammer candles, indicate that a cryptocurrency may see its value start to rise again before continuing down its current price path.

These patterns are great entry points for traders looking to capitalize on cryptocurrency price movements.

How can you use these pattern forecasts for your trading strategy? Use stop-losses.

Traders should never leave all their eggs in one basket – and stop-losses help ensure they don’t have to.

A stop-loss is an order placed with your broker to sell when a coin reaches a certain price.

This can be helpful if you’re worried about watching your investment plummet overnight and not being able to do anything about it (if you’re not prepared).

7. Create a crypto-friendly financial plan

The most important thing to know is that you don’t have to be a financial expert to invest.

For starters, read up on how bitcoin works, how blockchain technology operates, and what cryptocurrencies mean for eCommerce.

It’s also important to note that cryptocurrency is more volatile than traditional stocks.

So it pays to diversify your portfolio among different tokens and cryptocurrencies (using a service like Binance) rather than investing in just one token or currency.

And finally, because cryptocurrency transactions are encrypted on blockchains (ledgers of transactions), they provide added security when making payments online.

In other words, cryptocurrency investments may help keep your bank account safe from hackers – which means everything these days.

Conclusion

If you’re a new investor or looking to get into crypto, keep these tips and best practices in mind.

With some diligence and planning, you can be on your way to making big profits from small investments. Just remember to never invest more than you can afford to lose. Have a clear financial goal for your investment.

And finally, be patient and wait for opportunities. Do not chase short-term trends.

By following these guidelines, as investors, you will avoid common mistakes while maximizing your chances of success when trading cryptocurrency.