What the Worldwide Crisis Taught Us About Planning for the Worst-Case Business Scenario

An economic crisis is something no business owner wants to face, but it is a situation everyone should prepare for. Recent events have shined a bright light on the need to be ready for the worst-case scenario.

In a poll by the U.S. Chamber of Commerce, only 50 percent of small businesses report their business is in good health due to the current situation. Three in ten businesses have temporarily closed, and one in five say they will close permanently in two months or less.

Whether you had a business crisis plan prior to 2020 or not, now is the time to take action and put together a strategy for the unexpected. Here’s what business owners need to do to handle the current environment and to prepare for future economic downturns.

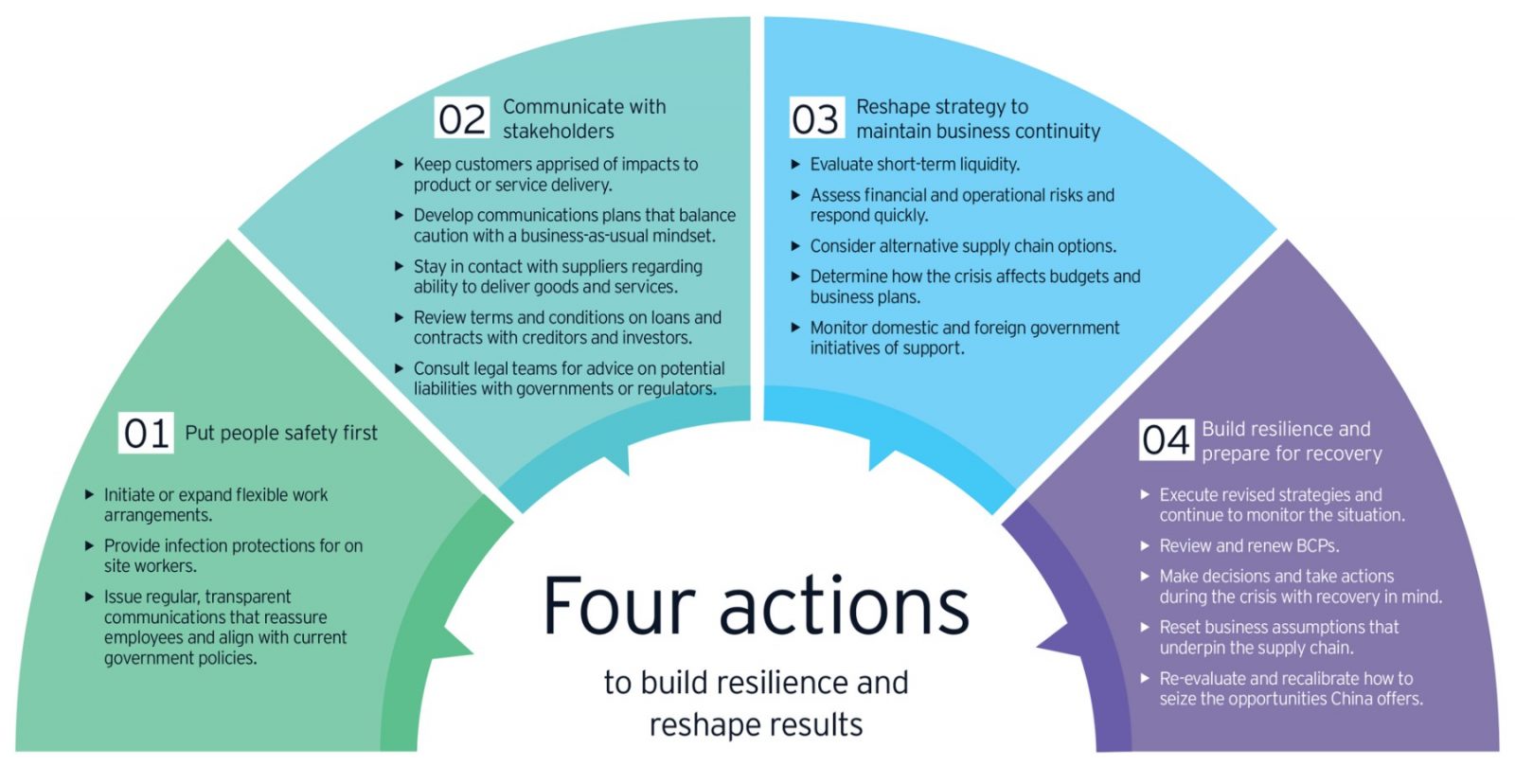

Source: EY.com

A good crisis management plan covers all your bases, from cash flow to chain of command. In an economic crisis, your plan will put the tools and resources you need to navigate uncertain territory at your fingertips. Rather than reacting in the moment, you’ll be ready to respond thoughtfully and rationally to help sustain your business through hard times.

The following steps are all part of building a solid crisis response plan that will help mitigate risks and get your business ready to weather the storm.

Build a Forecast for Economic Slowdowns

No one knows when a crisis will hit, but you can take steps right now to stay ahead of the curve and prepare for unexpected financial hardships. A crisis economy forecast combines your own specific business outlook with market trends to help you identify and prepare for future downturns. Get started with a two-step analysis:

- Identify and review your business’s KPIs. You need a firm understanding of how your business is currently performing to prepare for future economic hardship. Track your revenue, profit margins, cash flow and customer retention to get a picture of your overall financial health.

- Monitor key economic indicators. Business owners must watch the market like a hawk, noting fluctuations and seeking out downward trends. These are the warning signs of economic downturn, which include everything from GDP and consumer spending to employment statistics.

Review Your Insurance Coverage

If you approach insurance as a one-size-fits-all commodity, it’s time to change your perspective. You’ve likely already thought about your business’s physical coverage needs for property damage, but have you analyzed if filing for unemployment is an alternative? Other than that, here’s what you can do right now to make sure you’re ready:

- Sit down with your broker and go through the details of your policy. Consider add-ons such as business interruption insurance that will cover some of your losses if you or a provider/vendor unexpectedly shuts down.

- Seek out crisis-related discounts. This tip may apply to businesses impacted by our current situation, but can also help you design a strategy for future economic crisis. Currently, many insurance providers are offering discounts, refunds, or reduced premiums to businesses facing shutdowns or slowdowns related to the pandemic. This can free up some of your cash flow while still making sure you’re protected.

Plan for Business Continuity

Having a Business Continuity Plan (BCP) is vital. It lays out clear guidelines for how the business will continue to operate through uncertain times. While BCPs can take many forms, nearly all feature two key elements:

- Essential Operation Plan. In a worst-case scenario, what emergency measures will it take to continue operations? Consider your critical functions and determine what resources you will need to keep them performing, such as the number of employees, facilities, equipment, and cash flow. This will set up your bare-bones operating plan. Also, create a succession plan for the business, should you or other partners become incapacitated.

- Alternate Working Environments. A financial crisis can have serious repercussions for your physical operations. If you cannot maintain your current facilities, you’ll need a plan that will cut costs and keep you running. Consider your equipment and production needs and how you can meet those needs if you are unable to access your primary location. You may also save money by implementing a remote work strategy. Research the digital tools that will help facilitate this transition and have a plan in place.

Protect Your Records

An economic crisis can be widespread, or it can be confined to your business. Often, incidents of financial disaster for individual businesses are the result of compromised data. That’s why it is vital that your records are regularly maintained and protected. From hardware failure to cybercrime, there are several steps you can take to prevent a crisis:

- Be aware of the latest research and findings on data breaches and create a plan to address these scenarios. According to Verizon (PDF), small businesses were the largest victims of data breaches in 2019, with 69% of breaches perpetrated by outsiders and 16% by public sector entities. Hacking, social attacks, and malware were the top three ways data was breached.

- Update your antivirus and antispyware software and ensure they are running properly.

- Consider pulling together a digital crisis response team that will be ready to respond to cyber disasters.

- Educate your employees on proper and improper digital usage, make them aware of your policies,+ and monitor access to sensitive files.

Plan for Overall Business Success

All businesses and business owners have felt the impact of the pandemic in some form. Whether you’re struggling to reopen, adapting your product or service offerings to the current situation or just want to be ready for whatever the future brings, you can take steps now to prepare for an economic crisis:

- Monitor your credit score. The better your credit rating, the more likely you’ll be to qualify for loans and assistance when you need it.

- Diversify when it makes sense. The narrower your focus, the less you’ll have to offer your customers in crisis time. If you thoughtfully expand your product line, you may appeal to a broader audience.

- Stay true to core competencies. This is the flip side of the point above. Ideally, your business will strike a balance between diversifying — when risks are low and buyers are motivated — and remaining dedicated to your primary service or product offering.

It isn’t easy to predict and plan for a financial crisis, but it is one of the most important steps a business owner can take to protect and safeguard their business. Whatever happens to the market in the wake of the current situation and beyond, you can be ready for it by creating and implementing a solid economic crisis plan.

Author:

Wendi Williams is a freelance writer based in Indianapolis, IN, with over a decade of experience writing for a variety of industries from healthcare to manufacturing to nonprofit. When she isn’t working on solutions for her clients, she can be found spending time with her kids and husband, working in the garden, or doing more writing (of the fiction variety).

![Entrepreneurial Story of the Igwe Twins [Started as Office Cleaners]](https://thetotalentrepreneurs.com/wp-content/uploads/2016/09/Entrepreneurial-Story-of-the-Igwe-Twins-Started-as-Office-Cleaners-SpeedMeals-Mobile-Kitchen.png)