The 50/30/20 Rule – Does It Work for Business Budgets, Too?

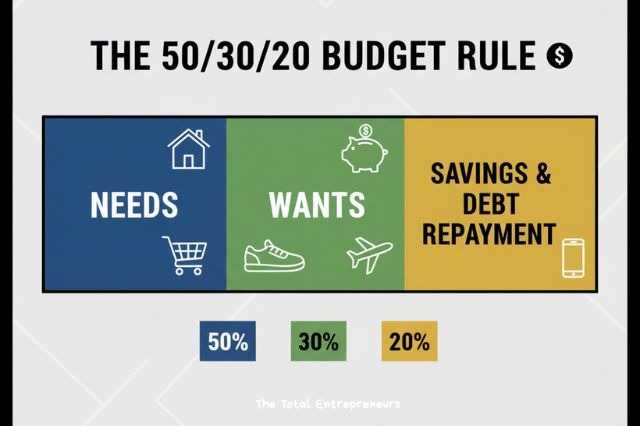

The 50/30/20 rule is a popular budgeting method for personal finance: Allocate 50% of income to needs, 30% to wants, and 20% to savings or debt repayment. But could this same framework apply to your small business budget?

While the core concept wasn’t designed for business use, it can offer a simple starting point for understanding where your money goes—and where it should go. Let’s walk through how the 50/30/20 rule could translate to a business setting and what adjustments you might need to make along the way.

Adapting the 50/30/20 Rule for Business

The original rule breaks down expenses into three clear categories:

- 50% Needs: Essential costs that keep things running

- 30% Wants: Nonessential spending that improves growth or comfort

- 20% Savings/Debt: Future-proofing or paying down obligations

For businesses, these categories can serve as a flexible guide. You won’t use the exact same percentages, but the structure helps you think intentionally about your spending habits.

What Counts as a Business “Need”?

The “needs” category covers the baseline costs required to operate. These are the non-negotiables—expenses that keep your doors open or your services running. Depending on your industry, this might include:

- Rent or mortgage for your workspace

- Utilities and internet

- Inventory or materials

- Insurance premiums

- Software or tools essential to operations

- Employee wages and payroll taxes

Calculating payroll correctly is especially important as it often represents your biggest ongoing expense. A payroll expense calculator helps you identify the true cost of each employee, including benefits and taxes—not just base pay.

Once you have a clear view of your fixed, unavoidable expenses, you can see how much room remains for growth-focused or discretionary spending.

Defining “Wants” in a Business Context

In personal budgeting, wants are the extras—streaming subscriptions, dining out, entertainment, etc. For businesses, “wants” translates to spending that isn’t strictly essential but adds value, efficiency, or appeal. Examples include:

- Advertising campaigns or upgraded branding

- Team-building retreats or office perks

- Premium software features

- Hiring consultants or coaches

- Attending industry conferences

These expenses aren’t vital to keeping your business alive, but they help you grow, attract clients, or retain employees. While it’s tempting to cut “wants” entirely in lean months, investing here wisely can actually improve your bottom line in the long term.

The 20%: Savings, Debt, and Safety Nets

The final 20% is about preparing for the future. In a business budget, this includes:

- Paying down business loans or lines of credit

- Setting aside emergency funds

- Saving for equipment upgrades or expansion

- Building reserves for tax payments

Many small businesses struggle because they don’t leave room for financial cushions. One unexpected expense—like equipment failure or a delayed invoice—can put cash flow at risk. Treating this 20% as non-negotiable helps you build long-term stability.

Rebalancing the Percentages

While the 50/30/20 split works well as a personal finance rule, small businesses often need to tweak it based on their stage, size, and industry. A startup with tight margins may spend 80% or more on essential needs, leaving little room for extras. That’s OK as long as you’re aware and adjusting intentionally.

Here’s a common small business adjustment:

- 70% Needs: Fixed costs like rent, wages, and utilities

- 20% Wants: Growth investments and team perks

- 10% Savings/Debt: Reserve funds, future spending, or paying down debt

The key isn’t to follow the 50/30/20 rule rigidly—it’s to use it as a framework for thinking about balance and long-term planning.

When the Rule Breaks Down

Some industries simply don’t fit neatly into these buckets. For example, manufacturers often spend a large percentage on inventory and machinery, leaving less flexibility. Seasonal businesses might have unpredictable income and need to allocate more toward reserves during peak months.

If your business doesn’t match the 50/30/20 idea, that doesn’t mean you’re budgeting wrong. It means you should build a structure that reflects your unique operations and risk tolerance.

Adding in Tax Responsibilities

Unlike personal budgets, businesses have an added layer of tax complexity. You need to plan for income tax, self-employment tax, payroll taxes, and possibly sales tax—depending on what you sell and where you operate.

Sales tax, in particular, can cause confusion if it isn’t calculated and collected properly. A simple tool on how to calculate sales tax helps ensure you’re charging the correct amount and not cutting into your profit margins by undercharging or absorbing those costs unknowingly.

Make sure tax obligations are factored into your “needs” category—because they’re unavoidable and the consequences of missing them are steep.

Also read: What Do You Need To Know About Tax And Tax Returns

Cash Flow vs. Budget Planning

One thing to remember: Budgeting isn’t just about where your money should go—it’s also about when it goes. Even if your percentages look right on paper, cash flow timing can disrupt the plan.

If a client pays late, you might have to pause marketing efforts or tap into savings to cover payroll. Having solid budgeting habits and a clear understanding of your cash flow calendar can help you prevent major disruptions.

Building a Budget That Actually Works

Whether or not the 50/30/20 rule fits your exact numbers, its core lesson holds true: Every dollar should have a purpose. Breaking your spending into categories encourages intentionality, planning, and financial health.

You don’t need to obsess over perfect ratios—but you should regularly review your expenses, track trends, and adapt your strategy as your business grows.

Start with a simple structure, customize it based on your needs, and commit to consistency. The clearer your budgeting system is, the easier it becomes to make confident decisions and build toward long-term success.